Redefining Digital Payments for a Borderless Economy

Redefining Digital Payments for a Borderless Economy

Payomatix is a Dubai-based PayTech company delivering secure, AI-driven, and scalable payment infrastructure designed to maximize authorization rates, reduce friction, and empower businesses to scale globally.

Payomatix is a Dubai-headquartered PayTech company delivering next-generation payment and embedded finance solutions to businesses across the UAE, GCC, and global markets. We provide a robust, scalable financial infrastructure designed to power seamless digital commerce. Our comprehensive suite includes multi-channel payment processing, intelligent payment orchestration, bulk payouts, white-label payment systems, and Banking-as-a-Service (BaaS) capabilities, enabling businesses to integrate financial services directly into their platforms.

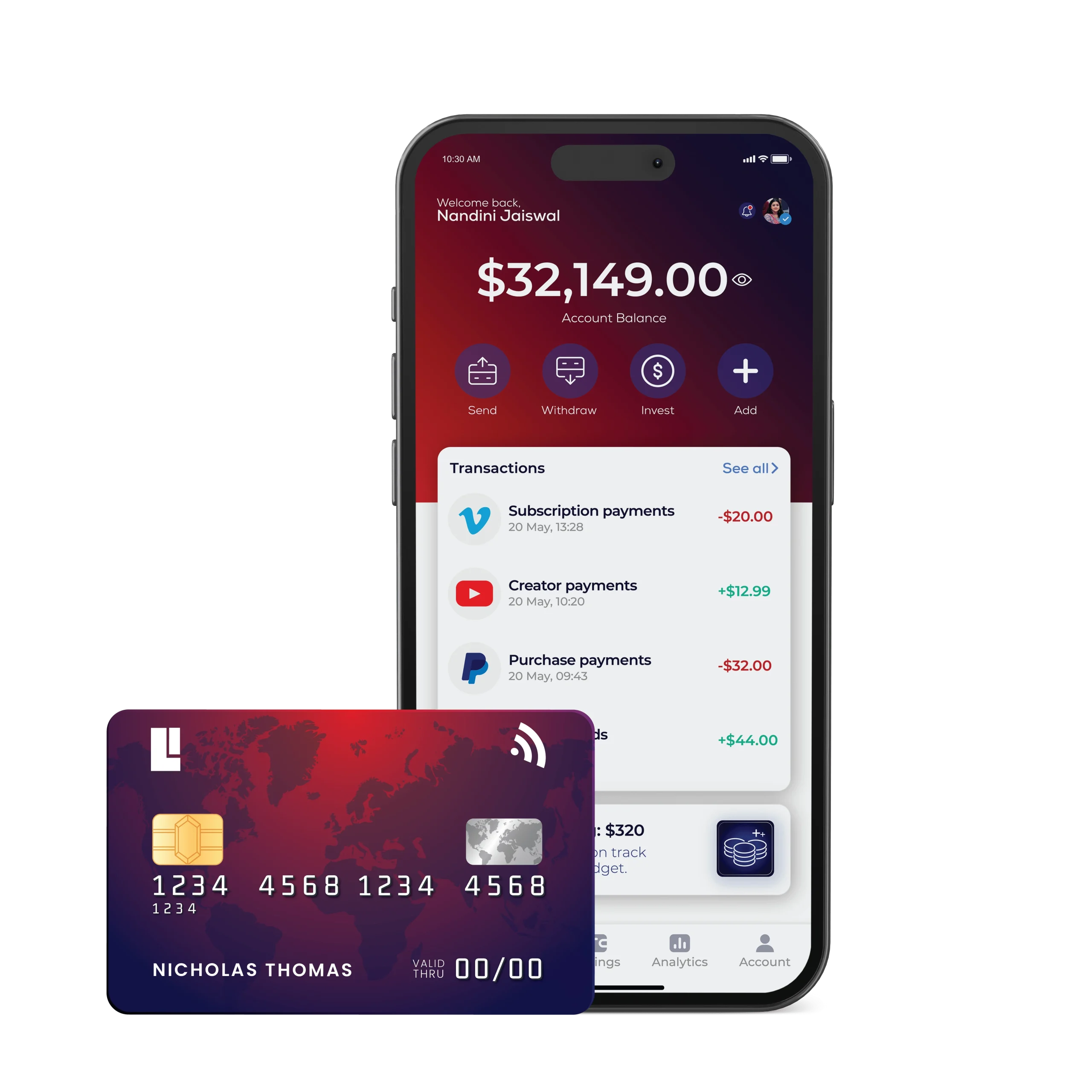

Payomatix is transforming the digital payments landscape through cutting-edge PayTech and Banking-as-a-Service (BaaS) capabilities. From seamless payment processing to embedded financial services, we enable businesses to integrate, manage, and scale financial operations effortlessly.

Built on secure, scalable infrastructure, our platform optimizes transaction success rates, supports multi-currency and cross-border payments, and empowers businesses to unlock new revenue streams through embedded finance.

Multiple Payment Methods

Accept cards, UPI, wallets, and net banking through a single integrated payment system.

Smart Payment Routing

Reduce failed transactions with AI-driven routing and secure payment processing for faster, reliable transactions.

Seamless Integration

An API-first approach with no downtime, ensuring smooth and efficient payment gateway integration.

Our Solutions

Unified PayTech Solutions Tailored for Your Business.

Payment Processing

Enable seamless, secure transaction processing across global cards, digital wallets, and alternative payment methods with real-time multi-currency capabilities.

Payment Orchestration & Aggregation

Optimize transactions with AI-powered smart routing, auto-failover, and aggregated acquiring networks for higher approval rates and enhanced payment performance.

White-Label & BaaS Services

Launch your own branded payment and embedded finance solutions with full customization, Banking-as-a-Service (BaaS), and compliance-aligned infrastructure.

At Payomatix, we are redefining the digital payments ecosystem by delivering intelligent PayTech infrastructure built for global commerce. We empower businesses with secure, scalable payment processing and advanced orchestration capabilities designed to optimize performance and drive sustainable growth.

Our mission is to simplify complex payment flows, enhance authorization rates, and enable businesses of all sizes to scale confidently through cutting-edge financial technology.

AI-Driven Smart Routing Technology

Our proprietary AI-powered Smart Routing engine strengthens payment orchestration and aggregation by dynamically optimizing transaction flows across multiple acquiring partners reducing declines and maximizing approval rates.

PCI-DSS Compliance & Secure Infrastructure

Backed by PCI-DSS compliance, international regulatory alignment, and advanced fraud prevention frameworks, Payomatix ensures secure, resilient payment processing with enterprise-grade reliability and risk management.

At Payomatix, we believe that payments should be effortless, not overwhelming. That’s why we’ve built a unified, intelligent, and seamless omnichannel payment solution that removes complexities and makes transactions faster, smarter, and more efficient.

Whether you’re a startup, an enterprise, or a financial institution, we offer enterprise payment solutions tailored to meet your unique payment needs.

Payomatix has transformed the way we handle transactions. Their payment switching platform with smart routing technology significantly reduced payment failures, and our customers love the smooth checkout experience. We’ve seen a 20% increase in successful transactions since switching to Payomatix!

Amit Sharma

CEO

As a fintech startup, we needed a scalable and secure payment processing solution that integrates effortlessly. Payomatix’s developer-friendly payment gateway API made integration seamless, and their fraud prevention tools give us peace of mind. Highly recommended for businesses looking for a next-gen payment gateway!

Priya Mehta

Co- Founder

We run a high-volume food delivery business, and quick payments are crucial. Payomatix’s omnichannel payment solution, including UPI and real-time settlements, has streamlined our operations and ensured faster payouts for our delivery partners. A game-changer for businesses needing instant transactions!